What I'm thinking about: After analyzing tens of thousands of land transactions, we continue to discover new layers of complexity in the underwriting process.

You might believe your systems are refined, your team is experienced, and your comparable analysis is nearly scientific—but the land market inevitably presents scenarios that expose gaps in your methodology.

And frankly? This ongoing challenge is what makes the business compelling.

Case in point: We're currently evaluating an East Texas rural property spanning over 20 acres at $3,000 per acre.

Recent sales in this area range from approximately $4,000 to $7,500 per acre—nearly a 2x spread within the same general market.

Which valuation should guide your underwriting?

This question reveals where many land investors—including seasoned professionals—overestimate their analytical precision.

The Limitations of Simple Price-Per-Acre Averaging

Using the example above, averaging all comparables yields roughly $5,200 per acre for your exit assumption.

Enter that figure into your model and move forward.

(While this approach seems overly simplistic, I observe it regularly—from real estate agents to land investors to institutional lenders with supposedly rigorous appraisal processes.)

More often than not, averaging price-per-acre produces inflated valuations relative to the subject property's actual market value. While some investors miss opportunities by being overly conservative, that scenario is uncommon in our experience.

Property-specific characteristics and current market dynamics determine value. "Current" means today's conditions—not data from 12 months ago, and certainly not 24-36 months prior.

In today's buyer-favorable market (broadly across the U.S., though real estate remains hyperlocal), margin for error has narrowed considerably.

Our Comparative Analysis Methodology

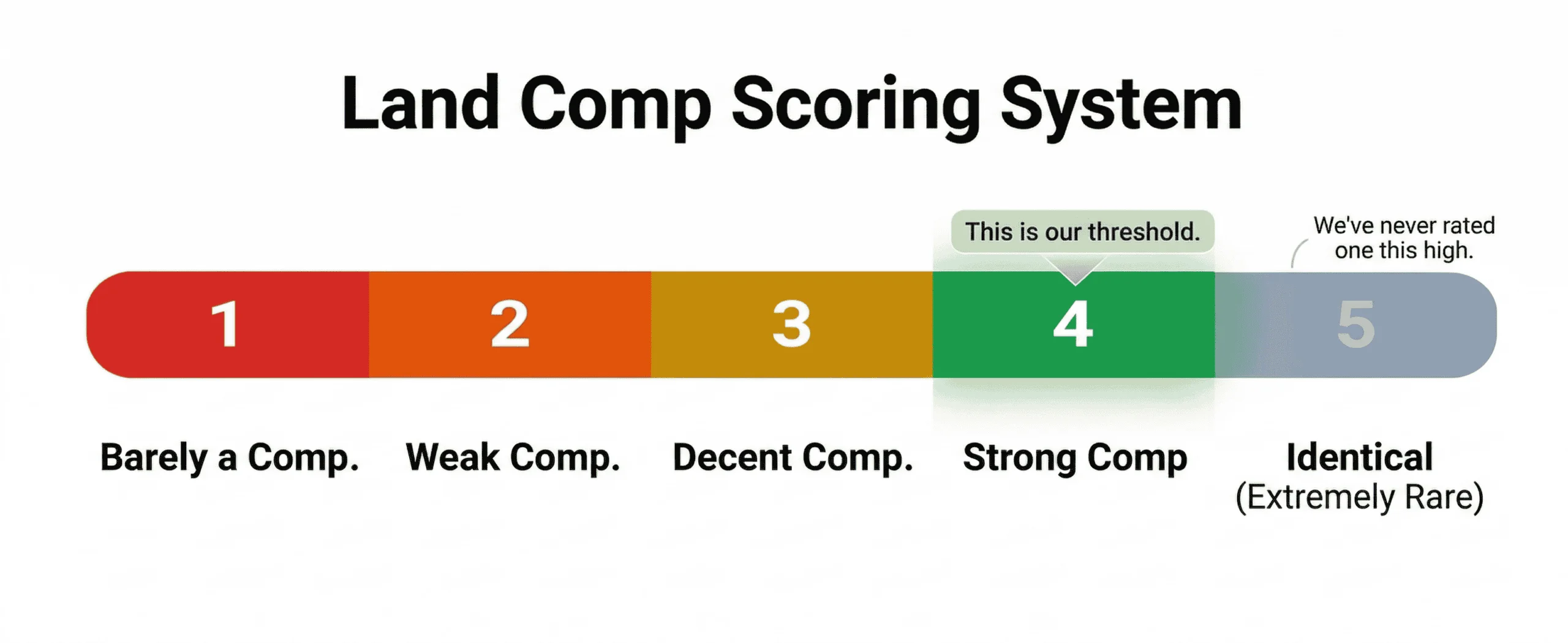

We employ a 1-5 ranking system in our due diligence questionnaire, or DDQ (available here), which mathematically weights pricing based on comparable quality.

The ranking structure:

- Rank 1: Marginally relevant, included for context only.

- Rank 2: Weak comparable with significant characteristic differences.

- Rank 3: Adequate comparable with several notable differences.

- Rank 4: Strong comparable with minor differences only.

- Rank 5: Nearly identical to the subject property.

Here's the reality: After thousands of property evaluations using this framework, we've rarely assigned a rank of 5. (Such properties typically exist in uniform subdivision markets, which generally fall below our funding thresholds.)

At best, comparables achieve a rank of 4, with subtle differences remaining (such as lot configuration, neighborhood quality, or road frontage).

While this scoring involves subjective judgment requiring team calibration, the difficulty of achieving high scores reflects the nuance required for accurate valuation.

Comparable weighting receives my most intensive review before funding approval. Without at least one rank-4 comparable—particularly a recent sale or pending transaction—the risk is too high unless the discount is exceptional.

Non-Disclosure States Compound the Challenge

In non-disclosure states like Texas, sold prices aren't accessible through public records.

We've developed an algorithm estimating sold prices using days on market, time between price reductions and pending status, and other factors—but actual data is irreplaceable.

We consistently send our sold comparables to our realtor for MLS verification. Our estimates are sometimes accurate and sometimes significantly off.

(Note that exit pricing can only be confirmed for MLS transactions. Off-market sales without conventional financing remain hidden.)

Many investors accept a comparative market analysis (CMA) from a realtor, but you or your team should always prepare your own analysis. I can count on one hand the times a realtor—even experienced ones—has prepared a comparable list matching our internal quality and thoroughness.

When your capital is at risk, no one will care as much as you. Trust, but verify.

For sold comparables where our realtor represented either party (we typically engage realtors based on recent market success), we thoroughly question the sale circumstances and how property characteristics compare to our subject property.

For this East Texas property, we needed to answer several critical questions:

- What constitutes "clearing" in this market? Our realtor suggested mulching and clearing a home site for $4,000. We showed the realtor photos of cleared comparables that sold at ~$7,500 per acre and confirmed our contractor could match that quality at the quoted price.

- What are the true utility costs? Most comparables have public water access. Without it? Wells cost $25,000 or more locally—a substantial cost that dramatically impacts value and could eliminate anticipated profitability.

- Where exactly is water access located? We contacted approximately 5-6 entities (including the local volunteer fire department) to confirm public water access for the subject property. Despite three comparables on the same highway having water, we conducted independent verification.

- How long did comparables remain on market? One comparable took 500+ days to sell. Another sold in 17 days. Weighted rankings differed for each, with our subject property more closely resembling the 17-day sale—a critical distinction when pricing for a 3-6 month exit.

- What is the vegetation quality? The subject property has mature, aesthetically appealing trees, compared to a sold comparable only four years into timber regeneration (difficult to discern aerially, but our realtor noted this having listed that property).

This isn't busywork. This is the difference between profit and loss.

This is why, even after funding over $6 million in land deals with 41% operating margins, we continue learning from every property.

Maintain curiosity. Ask every question until none remain. Trust and refine your process.

Our Valuation Conclusion

Based on detailed, feature-by-feature analysis of every comparable relative to the subject parcel (the clearing we're adding, the superior trees, the better buildability and location relative to population centers), we're valuing this property at $6,000 per acre.

Not the $5,200 mean. Not the $7,500 top-end comparable. Not the $4,000 worst-case scenario.

Could we be wrong? Certainly—we have been before and will be again. But we price for downside scenarios. We ensured no foreseeable scenario where the property would sell below $4,000 per acre before considering improvements.

Rule #1 in investing (any asset class): Don't lose money.

We've done everything possible to ensure we're not missing critical factors.

That's the process. Every single time.

Why This Market Builds Better Investors

As frequently noted in this newsletter and mainstream media, this is a challenging real estate environment.

Buyer inquiries are down. Properties sit longer. Without precise underwriting, losses are inevitable.

Remember that this is the ideal environment for skill development, because what works in a down market works even better in a bull market.

Conservative underwriting. Meticulous attention to detail. Triple-checking assumptions before wiring funds.

Before the wire goes out, you can always decline. Once it's sent? No reversals.

This is when you build credibility. This is how you demonstrate staying power.

And when the market turns? You'll still be operating.

The Infinite Game

Underwriting isn't a skill you master once and move on from.

It's an infinite game. Every deal provides new lessons. Every market shift reveals additional complexity.

The operators who understand this (who respect fundamentals, who keep investigating, and who don't assume they've figured everything out) are the ones who succeed long-term.

We're playing the 50+ year game. The investor with the longest time horizon wins.

If you're an experienced operator with consistent deal flow seeking a capital partner who thoroughly examines every detail to ensure accurate underwriting?

Send us your best deals. We write checks for $50,000 or more. We close 100% of committed deals. And we bring national underwriting experience to every transaction.

Let's grow together.

Get Your Property Analyzed Today

Originally published at https://seriousland.capital on December 22, 2025.

The post The Infinite Game of Land Underwriting appeared first on REtipster.